Table of Contents

- Understanding Invoice Financing

- Benefits for Small Businesses

- Technological Advancements in Invoice Financing

- Real-World Applications

- Considerations and Best Practices

- Conclusion

Invoice financing has become a pivotal option for small business owners seeking to maintain operational stability. By converting accounts receivable into cash, companies can access immediate funds to continue daily operations and support expansion without waiting for customer payments. Services that provide working capital against receivables have dramatically changed how businesses approach cash flow challenges. Rather than struggle through periods of delayed payment, companies can focus on growth and efficiency.

The modern economic environment requires agility and quick decision-making, and invoice financing offers a solution by bridging the payment gap between delivering goods or services and receiving customer payments. This funding strategy not only keeps businesses running but also enables them to seize new opportunities, adapt to market changes, and manage financial obligations. Owners can now invest in technology, add staff, and consistently meet payroll.

Understanding Invoice Financing

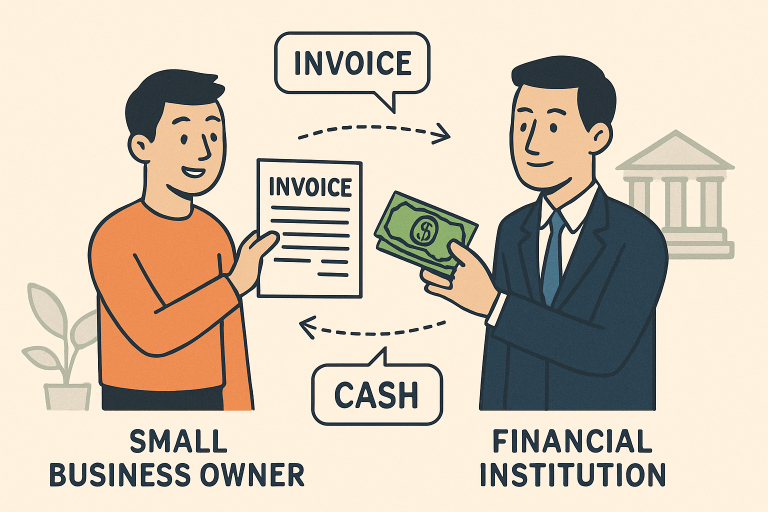

Invoice financing is a process where businesses sell outstanding invoices to a third-party financier at a discount in exchange for immediate payment. This arrangement allows companies to access funds tied up in receivables without waiting for customers to pay within their credit terms. Businesses pay a fee for this service, but the primary advantage is consistent cash flow, crucial for meeting ongoing expenses and obligations. Industries that deal with large contracts or long payment terms, such as manufacturing, wholesale, and professional services, often find invoice financing especially beneficial.

There are two main types of invoice financing: factoring and invoice discounting. Factoring involves selling invoices to a financier, who then takes responsibility for collecting payment from customers. Invoice discounting, on the other hand, keeps the responsibility for collecting payments with the business while using invoices as collateral for a cash advance. Both models support liquidity and add flexibility to small businesses’ financial toolkit.

Benefits for Small Businesses

- Improved Cash Flow:Companies can convert receivables into cash more quickly, enabling them to pay suppliers, cover payroll, and meet other expenses without the strain of cash flow gaps.

- Growth Opportunities:With quick access to funds, businesses are better positioned to take on new projects, hire more employees, and upgrade technology or equipment, fueling further growth.

- Credit Risk Mitigation:By transferring some or all of the risk of non-payment to the financing partner, businesses protect themselves from the adverse effects of late-paying or defaulting clients.

- Enhanced Credit Rating:Consistent cash flow allows businesses to meet financial obligations on time, helping maintain, or even improve, their credit rating and reputation with lenders.

According to Forbes, many startups and small companies in fast-growing sectors have turned to invoice financing as a more accessible option compared to traditional loans, which often require collateral and lengthy approval processes.

Technological Advancements in Invoice Financing

The invoice financing sector has seen a rapid digital transformation. Modern platforms now integrate directly with accounting and enterprise resource planning (ERP) systems, such as Sage and Acumatica. This seamless integration means businesses can automatically upload invoices and request financing, cutting down administrative time and reducing errors. For instance, fintech innovators like Nuvei enable merchants to access invoice financing directly through their ERP dashboards, allowing for quicker funding decisions and streamlined operations.

Machine learning and artificial intelligence are increasingly used to assess credit risk and determine invoice eligibility in real time. This accelerated assessment speeds up the application process, making it easier for even the smallest businesses to qualify for financing without extensive paperwork.

Real-World Applications

In sectors ranging from logistics to creative industries, invoice financing is being used to drive business forward. One prominent example is home-based businesses, which make up a significant segment of the small-business landscape. Companies like 1st Commercial Credit offer tailored solutions for these businesses, providing the liquidity needed to cover daily expenses and pursue growth opportunities. This flexibility is critical in industries where project-based work or seasonal demand can produce uneven revenue streams.

Larger enterprises have also begun leveraging invoice financing to optimize their own working capital strategies, using these tools not only for survival in difficult times but also for strategic investment and scalability. Insights from the Wall Street Journal highlight how banks and fintech companies alike are innovating in lending and invoice finance, making funding more accessible for small business owners.

Considerations and Best Practices

While invoice financing brings many benefits, savvy business owners must carefully weigh their options to maximize value. Key considerations include:

- Cost Analysis:Carefully assess all fees, rates, and contract terms to ensure the arrangement is cost-effective for your specific business situation.

- Customer Creditworthiness:Since a financier will review your customers’ credit profiles, maintaining solid, dependable commercial relationships is crucial for ongoing access to financing.

- Regulatory Compliance:Stay up to date on financial regulations at the local and national levels to avoid compliance issues and safeguard your business’s operations.

Conclusion

Invoice financing serves as a strategic funding option for small businesses seeking stability and sustained growth in competitive, fast-moving markets. By converting outstanding invoices into immediate working capital, companies can improve cash flow without taking on traditional debt. This accessible funding allows business owners to cover payroll, invest in inventory, launch marketing campaigns, and seize expansion opportunities without waiting for customer payments. It also reduces the strain caused by slow-paying clients and seasonal revenue fluctuations. When paired with disciplined cost control, careful customer credit evaluation, and regulatory compliance, invoice financing empowers entrepreneurs to strengthen operations, manage risk effectively, and build more resilient, future-ready businesses.